When you pick up a generic pill at the pharmacy in Berlin, Paris, or Warsaw, you might assume it’s identical to the brand-name version. But behind that simple exchange is one of the most complex regulatory systems in the world. The European Union doesn’t have one single rule for generic medicines-it has four different pathways, each with its own timeline, cost, and hurdles. And in 2025, those rules changed dramatically. If you’re trying to understand why some generics hit shelves quickly while others take over a year to appear, you need to know how the EU’s system actually works.

Four Ways to Get a Generic Drug Approved in the EU

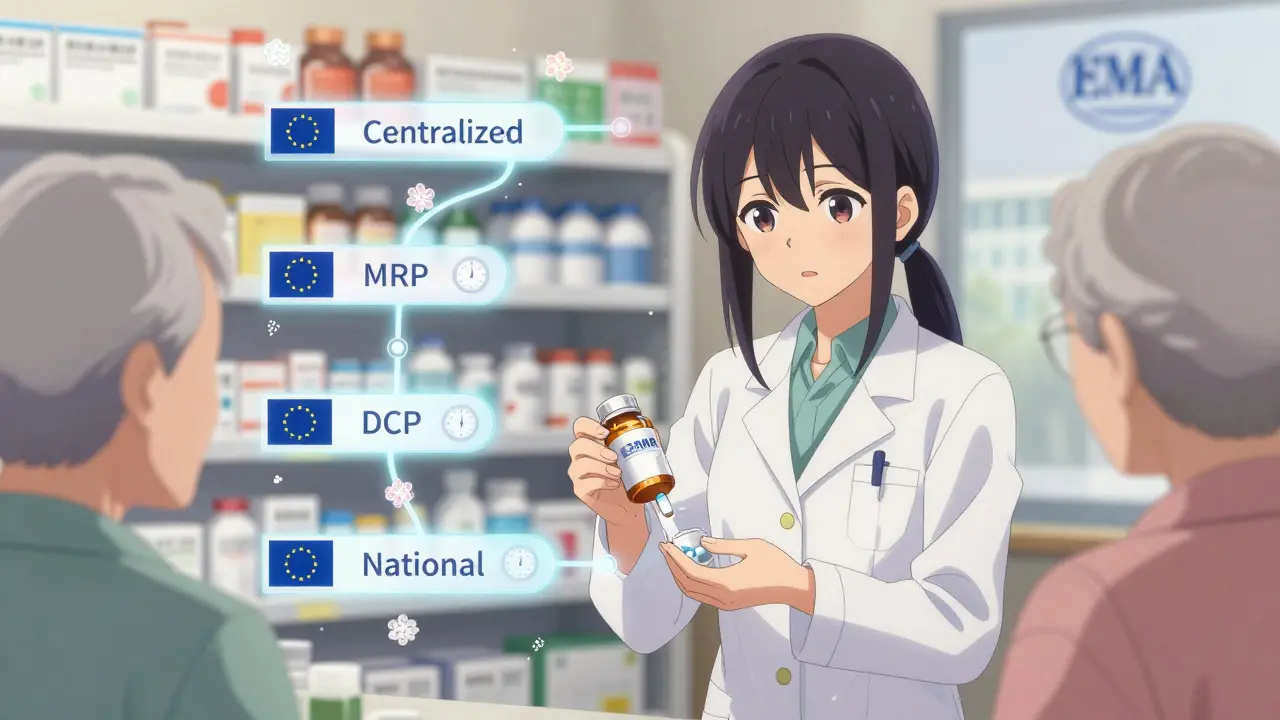

The EU doesn’t force every generic drug through the same process. Instead, manufacturers choose from four distinct approval routes, each suited to different business goals. The Centralized Procedure is the fastest way to get a generic approved across all 27 EU countries, plus Iceland, Liechtenstein, and Norway. It’s used for about 15% of applications. The application goes directly to the European Medicines Agency (EMA), which reviews it in 210 days-cutting to 180 days under the 2025 reforms. If approved, the drug gets a single marketing authorization valid everywhere. But it’s expensive: application fees alone cost around €425,000, with total consultancy and preparation costs pushing €1.2-1.8 million. That’s only worth it for high-value generics expected to generate over €250 million in annual sales.

The Mutual Recognition Procedure (MRP) is used for 42% of applications. Here, a company gets approval in one country-the Reference Member State-and then asks others to accept it. Sounds simple, right? Not quite. While the official timeline is 90 days for consensus, the average takes 132.7 days. Why? Because countries like Germany, France, or Italy often demand extra data, even if the EMA already approved it. Teva’s 2023 launch of a generic rosuvastatin shows how this plays out: the drug got technical approval in Germany, but pricing negotiations dragged on for over eight months, delaying availability in the Netherlands and Belgium.

The Decentralized Procedure (DCP) lets companies apply to multiple countries at once, without needing prior approval anywhere. It’s popular because it avoids the upfront cost of the Centralized Procedure. But it’s messy. Thirty-seven percent of DCP applications face delays longer than six months. Why? Because Eastern European authorities sometimes interpret quality standards differently. One company might submit the same stability data to Poland and Romania, only to get rejected in one for reasons the other accepts. This inconsistency adds months to timelines and unpredictability to supply chains.

The National Procedure is the least common-only 5% of applications use it. It means applying to just one country. It’s slow, taking 180 to 240 days, and gives you no cross-border access. But it’s still used strategically. Accord Healthcare, for example, used this route in France in 2024 to target a high-reimbursement market. Even though it took 197 days, they avoided the coordination headaches of the MRP or DCP. For niche products or markets with unique pricing rules, it’s sometimes the smartest path.

What Makes a Generic “Equivalent”?

Before any of these pathways even start, the drug must prove it’s the same as the original. The EMA requires three things: identical active ingredients, the same pharmaceutical form (tablet, injection, etc.), and proven bioequivalence. Bioequivalence means the body absorbs the generic at the same rate and extent as the brand-name drug. To prove this, manufacturers run clinical studies on healthy volunteers. The data must show that the generic’s concentration in the blood-measured by Cmax and AUC-falls within 80.00-125.00% of the original. That’s not a suggestion; it’s a hard requirement. If the numbers are outside that range, the application is rejected.

But here’s where it gets tricky. Some generics are more complex than others. Inhalers, for example, aren’t just about chemical composition-they involve delivery mechanisms. Germany’s BfArM now requires additional pharmacodynamic studies for these, beyond what the EMA mandates. That means even if a generic passes the EMA’s test, it might still get stuck in Germany. A 2025 ABPI survey found 68% of generic manufacturers listed inconsistent bioequivalence requirements as their biggest regulatory headache.

The 2025 Pharma Package: What Changed?

The biggest shift happened on June 4, 2025, with the finalization of the EU Pharma Package. This wasn’t a tweak-it was a rewrite of the rules governing how generics enter the market. The most important change? The expanded Bolar exemption. Before 2025, companies could only start pricing and reimbursement talks with health authorities 2 months before a patent expired. Now, they can start 6 months before. That might sound small, but it cuts an average of 4.3 months off the time between patent expiry and market launch. REMAP Consulting estimates this alone will speed up access for over 70% of upcoming generics.

Another major change: Regulatory Data Protection. Previously, generics couldn’t rely on the originator’s clinical data for 10 years. Now, it’s 8 years of data protection, plus 1 year of market exclusivity-extendable to 2 years if the drug meets public health goals. This means generics can start using the original data sooner, but they still can’t sell for a full year after approval. It’s a balance: more competition, but still some protection for innovators. The European Generic and Biosimilar Medicines Association (EGA) says this creates a more dynamic market without killing innovation.

But not everyone is happy. Professor Panos Kanavos from LSE Health warns that the 1-year market exclusivity might discourage investment in complex generics-like biosimilars for rare diseases-because the return isn’t big enough. Meanwhile, the new €490 million sales threshold for Transferable Exclusivity Vouchers could hurt mid-sized companies. If you’re not selling €490 million worth of a drug, you can’t trade your exclusivity rights. That favors giants like Sandoz or Viatris over smaller players.

Real-World Impact: Who Wins and Who Loses?

The numbers tell a clear story. In 2024, generics made up 65% of all prescriptions in the EU by volume-but only 18% by value. That gap shows how cheap generics are, even when they’re widely used. The EU generics market was worth €42.7 billion in 2024, up 6.2% from 2023. India now accounts for 38% of all approvals, up from 29% in 2020. That’s because Indian manufacturers have mastered the MRP and DCP systems, often undercutting European firms on price.

But European companies aren’t giving up. Sandoz used the Centralized Procedure to launch a generic version of Novartis’s Cosentyx in Q2 2025. The result? Simultaneous launch across all EU countries-11 months faster than the MRP would have allowed. That’s the power of choosing the right pathway.

Meanwhile, the Critical Medicines Act of March 2025 added another layer: mandatory stockpiling of 200 essential generics. This is meant to prevent shortages, but it also adds new quality checks. Companies now need to prove they can maintain supply even during disruptions. That raises the bar for entry, especially for small manufacturers.

What Manufacturers Must Do Now

Preparing for approval isn’t just about paperwork anymore. The 2025 reforms require new skills and systems. By 2026, all product information must be submitted electronically in XML format (ePI). That’s not a suggestion-it’s a legal requirement. Companies without the right IT setup will be blocked. White & Case estimates this change will cost €180,000-250,000 per firm to implement.

Preparation time has also increased. A Centralized Procedure submission now needs 15-18 months of lead time, with 6-8 months dedicated just to bioequivalence studies under the updated 2025 EMA guidelines. Regulatory teams need to know not just EU rules, but national quirks. France requires pediatric formulation details. Germany demands extra stability data for polymorphic compounds. The EMA offers a free Q&A portal, but a 2025 survey found 58% of companies got conflicting answers from national authorities-especially on impurity limits for older drugs.

It’s no longer enough to have a good generic. You need a smart strategy. Choose the wrong pathway, and you lose months-or even years. Ignore national requirements, and you get rejected. Underestimate the cost of compliance, and you lose money before you even launch.

What’s Next?

The next big milestone is July 1, 2026, when the revised Regulatory Data Protection rules fully take effect. That’s when the 8+1 (or 8+2) system kicks in for all new applications. Evaluate Pharma predicts this will speed up entry for 78 high-value biologics currently in development.

Long-term, the reforms aim to cut the 22.4-month gap between U.S. and EU generic launches. Canada, by comparison, closes that gap in just 8.7 months. The EU is still behind, but the 2025 changes are moving the needle. REMAP Consulting forecasts medicine shortages will drop by 35% by 2028 thanks to the new obligation-to-supply rules.

But challenges remain. Fragmentation hasn’t disappeared. National authorities still interpret rules differently. The system is more efficient than before, but it’s still a maze. The winners? Companies that invest in regulatory expertise, choose their approval pathway wisely, and plan ahead. The losers? Those who treat the EU as one market when it’s still 27 different systems under one umbrella.

Why do some generic drugs take longer to appear in certain EU countries?

Even if a generic is approved by the EMA, individual countries can delay its market entry through pricing negotiations, reimbursement rules, or additional local requirements. For example, Germany may demand extra stability data, while France may require pediatric formulation details. These national variations mean a drug approved in one country can be held up for months in another.

What’s the difference between the Centralized and Mutual Recognition Procedures?

The Centralized Procedure gives a single approval valid across all EU countries and is managed directly by the EMA. It’s faster for market access but costs over €1.5 million. The Mutual Recognition Procedure starts with approval in one country, then asks others to accept it. It’s cheaper (€180k-220k) but slower, with delays from national objections. MRP is better for mid-range products, while CP is best for high-value generics.

Can a generic drug be approved in the EU without clinical trials?

Yes-but only if it proves bioequivalence. Instead of repeating full clinical trials, manufacturers conduct bioequivalence studies on healthy volunteers, comparing blood concentration levels of the generic to the original drug. As long as absorption rates fall within 80-125%, regulators accept it as equivalent. This is why generics are cheaper: they don’t need to redo expensive Phase III trials.

How did the 2025 Pharma Package change the timeline for generic launches?

The biggest change was extending the Bolar exemption from 2 months to 6 months before patent expiry. This lets manufacturers start pricing and reimbursement talks earlier, shaving off an average of 4.3 months from launch time. Combined with shorter assessment periods (210 to 180 days for CP), the reforms are accelerating market entry across the EU.

Are Indian generic manufacturers dominating the EU market?

Yes, they’re gaining ground fast. In 2024, Indian companies secured 38% of all EU generic approvals, up from 29% in 2020. Their strength lies in mastering the MRP and DCP systems, offering lower prices, and scaling production efficiently. But European firms like Sandoz and Viatris still hold 52% of the market by leveraging the Centralized Procedure for high-value drugs.

So basically the EU turned a simple drug approval process into a bureaucratic obstacle course. Why not just have one standard? Everyone else manages. This overcomplication is why I don't trust European healthcare anymore.

And don't get me started on the 'national quirks'. If Germany needs extra stability data for polymorphic compounds, why not just standardize that? It's not like they're inventing new science here.

Indian manufacturers have cracked the code on MRP and DCP. We operate lean, we optimize logistics, and we understand regulatory nuances better than most European firms. The 38% approval share in 2024 isn't luck - it's execution. The EU system rewards efficiency, and we deliver.

For mid-tier players, the €1.5M CP cost is a non-starter. We don't need it. We're building volume, not vanity.

I swear to god I read this whole thing and still don't know if I'm supposed to be impressed or terrified.

So a generic drug can be approved but still sit on a shelf for 8 months because France wants pediatric details and Germany wants extra stability tests? That's not regulation. That's performance art.

And who's paying for all this? The patient? The taxpayer? The guy who just wants his blood pressure pill without a PhD in EU pharmacology?

I'm not surprised. Every time a government says 'we're streamlining,' it means they're adding more layers. The 2025 reforms? More like 2025 re-entanglement.

And that €490M threshold for transferable exclusivity vouchers? That's not market competition - that's corporate welfare for Big Pharma. Sandoz and Viatris win. Everyone else gets left in the dust. This isn't innovation. It's consolidation disguised as reform.

You say the EU is fragmented? Nah. It's actually the most unified system I've ever seen. All 27 countries are just doing their own thing under the same umbrella. That's not fragmentation - that's diversity.

And if Indian companies are dominating, maybe it's because they're better at playing the game. Maybe the EU's system isn't broken - maybe it's just too fair for lazy European firms.

I love how this post breaks down the pathways like a flowchart 🤓

Centralized = Ferrari, MRP = Prius, DCP = DIY IKEA furniture, National = that one weird cousin who only uses fax machines.

And hey - if you're a small company trying to launch a niche generic, maybe the 'slow' path is the smart one. Sometimes going slow is the fastest way to win. 🙌

This is actually really hopeful. The reforms are fixing real problems. The Bolar exemption extension alone? That’s a game-changer for patients waiting for affordable meds.

Yes, the system’s messy. But it’s getting better. We’re cutting 4.3 months off launch time. That’s 4.3 months of someone not paying $200 for a pill they could get for $5.

And the stockpiling mandate? That’s not red tape - that’s public health. We need to stop seeing regulation as the enemy. It’s the guardrail.

There's a deeper philosophical question here: Is medicine a commodity or a public good?

If it's a commodity, then the market should decide - and the €1.5M CP cost is just capitalism doing its thing.

If it's a public good, then why are we letting pricing negotiations in France delay access for patients in Belgium? Why are we letting regulatory fragmentation determine who gets their insulin on time?

The 2025 reforms are a step toward the latter - but we're still stuck in the former.

We need to ask: Who is this system really serving?

You think this is bad? Wait till you find out the EMA is secretly funded by Big Pharma. They approved 98% of applications last year. Coincidence? Or a backdoor for patent extensions?

And why is India getting 38% of approvals? Because they're dumping cheap generics with borderline quality. The EU is letting them in because they're too lazy to enforce their own rules.

Next thing you know, your blood pressure pill is made in a basement in Mumbai with unverified excipients. I've seen the reports.

The real issue? The EU still treats medicine like a national product, not a European one.

One system. One standard. One timeline.

Everything else is just noise. And noise costs lives.

ePI in XML by 2026? That's not innovation - that's a tax on small firms.

€250k to update your IT system? Most generics makers don't have that kind of cash.

This isn't modernization. It's a gatekeeping move. The big players will adapt. The rest? They'll vanish. And patients lose.

I just want to say thank you for writing this. It's so hard to find clear info on how generics actually work in the EU.

As someone who's watched a family member struggle with drug access across borders, this breakdown means a lot.

It's frustrating, yes - but also hopeful. Change is possible. And you showed us how. ❤️